Friday, 19 April 2024 06:19 AM

OR

Login using

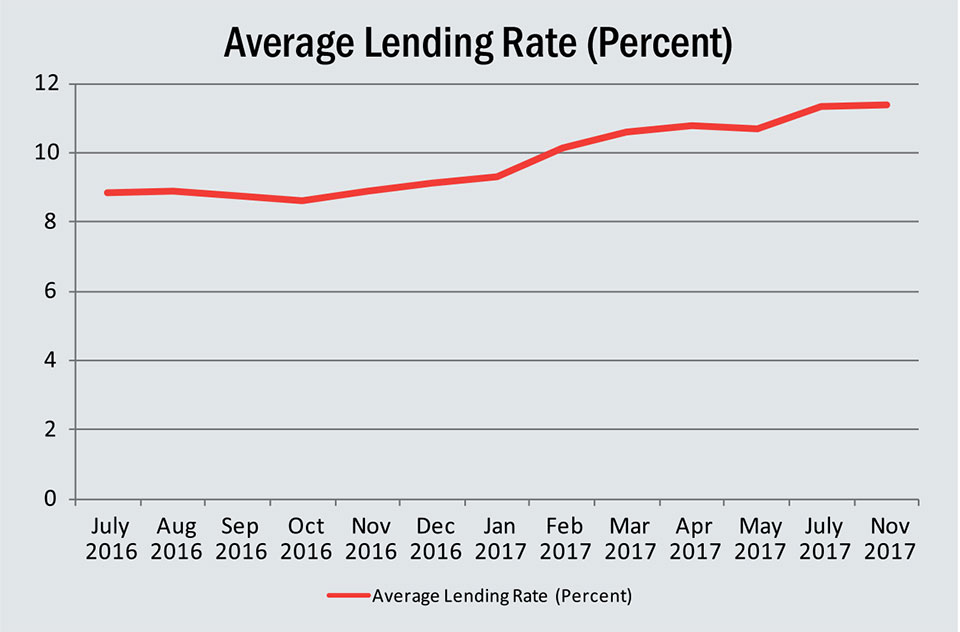

Credit crunch bedevils banks: Bank deposit rate at 13%, lending rate spikes to 16%

Published On: December 29, 2017 09:30 AM NPT By: Republica | @RepublicaNepal

Bankers' lack of farsightedness, aggressive lending blamed

KATHMANDU, Dec 29: Due to lack of farsightedness and aggressive lending practices among banks and financial institutions (BFIs), credit is getting very expensive for borrowers.

As lendable-fund-starved BFIs are in fierce competition to attract fresh deposits by offering higher interest rates, they are passing such higher cost on to their borrowers by charging them exorbitant interests. The deposit rates, particularly on fixed deposits, have already crossed double digits. Civil Bank Ltd on Thursday raised the fixed deposit rate to 12.22 percent for general public and joined the list of commercial banks increasing their deposit rates to attract funds. Many banks are collecting deposits from institutional depositors by offering them over 13 percent interest rates. Borrowers, particularly business firms, complain that BFIs have already jacked up lending rates by two to three percentage points. According to businesspersons, they are being charged up to 16 percent from BFIs on borrowing for business.

According to the data of the Nepal Rastra Bank (NRB), the interest rates are on a rising trend since the last two years. Since the interest rates charged by banks vary widely depending upon the types of loans and borrowers, the average rates may not reflect the real borrowing cost of the banking industry.

The sudden spike in the interest rates is a result of mismatch between the growth in deposits and loans of the BFIs. They are not allowed to lend more than 80 percent of what they have as core capital plus the deposit they have collected. Most of the banks are nearing the prudential lending limit and thus competing against each other to attract fresh deposits.

According to observers, the aggressive lending practice among the BFIs even when the deposit was rising at a very low pace has exacerbated the 'credit crunch'.

According to Nepal Bankers Association's latest data, lending of 28 commercial banks jumped 0.35 percent, or by Rs 7 billion, while their deposit base rose just 0.27 percent, or Rs 6 billion, in a week (between December 15 and December 22).

Many have attributed the aggressive lending practice among the banks to the pressure from their shareholders for higher dividends.

"We have been asking banks to increase lending cautiously. They seem to lack farsightedness in mobilizing resources," said Shiva Raj Shrestha, a deputy governor of the NRB.

Anal Raj Bhattarai, a banking expert, also agrees. "The problem has resulted from the banking practice of extending long-term loans from short-term deposits," said Bhattarai, who is also a member of the national coordination council at Confederation of Nepalese Industries. "These banks, which faced a similar problem last year, should have made arrangements for longer-term instruments and funds when the interest rates had gone down recently," he added. There had been some corrections on interest rates in the beginning of the current fiscal year when the NRB relaxed the prudential lending limit and the government's capital expenditure rose.

The 'credit crunch' is likely to worsen further because the deposit base of the BFIs will deplete when taxpayers withdraw deposits to the tune of Rs 60 billion for paying taxes by mid-January, the end of the second quarter of the fiscal year. The treasury surplus maintained by the government due to low capital spending coupled with slowdown in remittance inflow has put a dent in the growth of deposit volume of the BFIs.

Bank executives, however, defend the growth in lending, citing that their forecast was based on the government spending. "The lending target of banks was at a higher end as due to assumptions that the election spending, rise on capital spending and expenditures of local units will pump more cash into the banking system," said Gyanendra Dhungana, vice president of Nepal Bankers' Association (NBA).

You May Like This

Laxmi Bank raises interest rate of recurring deposit scheme

KATHMANDU, March 22: Laxmi Bank has increased the interest rate of 'Lakshit Muddati - Recurring Deposit' to 10 percent per... Read More...

Banks on lending spree despite slow deposit growth

KATHMANDU, Dec 28: Slow deposit growth has not restrained banks from ramping up their loan disbursements, indicating that lendable funds in... Read More...

Bank lending continues to rise, deposit base falls

KATHMANDU, May 10: Banks are struggling to attract deposits despite rise in demands for loans. ... Read More...

Just In

- Govt receives 1,658 proposals for startup loans; Minimum of 50 points required for eligibility

- Unified Socialist leader Sodari appointed Sudurpaschim CM

- One Nepali dies in UAE flood

- Madhesh Province CM Yadav expands cabinet

- 12-hour OPD service at Damauli Hospital from Thursday

- Lawmaker Dr Sharma provides Rs 2 million to children's hospital

- BFIs' lending to private sector increases by only 4.3 percent to Rs 5.087 trillion in first eight months of current FY

- NEPSE nosedives 19.56 points; daily turnover falls to Rs 2.09 billion

Leave A Comment